P1. The settlement price will be the price established by the VWAP algorithm for the contract month in question, based on valid trades as per the parameters stipulated in the table 1 of the Monthly Parameters.

P2. If procedure P1 cannot be applied, the settlement price for the contract month in question will be the average valid bid prices and valid ask prices with valid bid-ask spreads for that contract month as per the parameters stipulated in Table 1 of the Monthly Parameters Annex.

P3. If procedure P2 cannot be applied, the settlement price for the contract month in question will be calculated by summing (i) the settlement price for that contract month on the immediately preceding day to (ii) the price variation for the term corresponding to the contract month in question calculated by linear interpolation of the settlement price variation of the day over the immediately preceding day of the immediately previous and subsequent contract months with settlement price according to the equation described in the B3 Pricing Manual – Futures. The linear interpolation of the settlement price variation of the day over the immediately preceding day ensures that the settlement price for the contract months without notice fluctuates according to the fluctuation of the contract months that were traded.

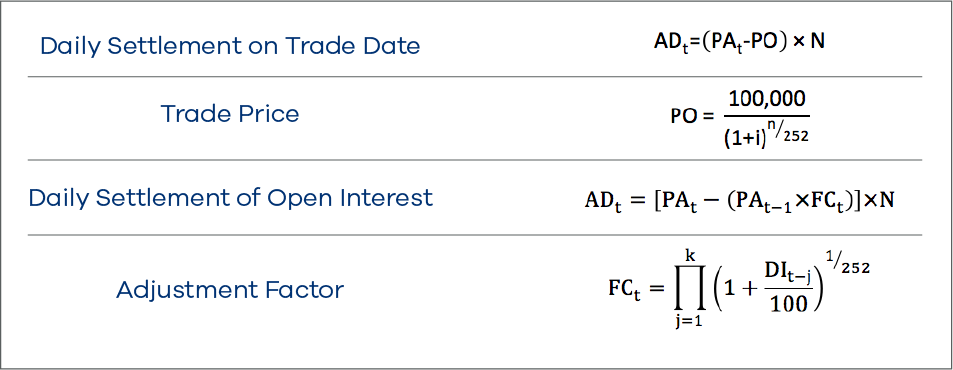

To view the calculation details, please refer to

P4. If procedure P3 cannot be applied due to the absence of a subsequent contract month with settlement price, then the settlement price for the contract month in question will be calculated according to the equation described in the B3 Pricing Manual – Futures by summing (i) the settlement price for this contract month on the immediately preceding day to (ii) the settlement price variation of the day over the immediately preceding day of the immediately previous contract month with settlement price. If the price obtained through this procedure does not follow a valid order price (i.e. the price is lower than a valid bid price or higher than a valid ask price), the settlement price will be the valid order price with the closest value. In this situation, this contract month (¿−1) will be considered a reference point for the second part of the equation described in the B3 Pricing Manual – Futures for all longer contract months.