Family of products

Listed derivatives contracts are grouped into families of products, based on each underlying asset. The same price tables will be applied to the same family. The volumes of all the contracts will be added together to apply reductions by volume.

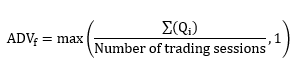

ADV calculation

Monthly ADV is calculated every month for each investor, considering all the accounts of a same document (CPF, CNPJ or third block of the CVM code) at all the brokerage houses. All the accounts linked to a same master account, regardless of the investor, will have their volumes consolidated in the master document linked to it.

The calculation is made by the sum of all the contracts traded in a same family (purchases and sales, day trade or not) between the first and the last business days of the previous month, divided by the number of trading sessions in the previous month. Each family of products has an ADV, which will be the average quantities adjusted by the weight of all the contracts of the family, with the calculation also being rounded off to zero decimal places:

Where:

ADVf = ADV of family of products f;

i = index that denotes each of the products in a same family;

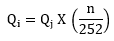

Qi = traded quantity of contracts of each product of the family on each day of the month. For families of product that have a term (Options on DI Futures, Options on IDI, Selic Rate), the trading volume shall be adjusted to the duration of the contract before multiplication by the weight:

Where:

Qi = adjusted number of contracts of each contract month;

Qj = traded number of contracts of each contract month;

n = nmber of trading days according to the table below:

| Family | n = dias de saque entre... |

|---|---|

| Selic Rate | trading date and expiration date of each contract |

| Options on DI Futures | expiration date of the option and of its underlying futures contract |

| Options on IDI | trading date and expiration date of each contract |

This calculation shall also be rounded off to zero decimal places.

In the first month that the investor trades it will be allocated to the first volume tier of the table.

Average cost calculation

Once the ADV of the family of products has been calculated, the next stage is calculation of the average cost for the exchange fees and for the variable registration fee appropriate for each family. This is a progressive calculation, weighting values by the total transactions of each tier, respecting each tier’s limits for the number of contracts

| Progressive table | ||

|---|---|---|

| Floor | Cap | Tier value |

| D1 | U1 | V1 |

| D2 | U2 | V2 |

| D3 | U3 | V3 |

| ... | ... | ... |

| Di-1 | Ui-1 | Vi-1 |

| Di | Ui | Vi |

| Dn | Un | Vn |

Average cost is defined as:

Where:

= calculated average cost;

= calculated average cost;

ADV = ADV calculated according to the previous item;

Ui = each tier's cap;

Un = last tier's cap;

Vi = value of the table associated to each tier;

Vn = value of the table associated to the last tier.

Each of the fees is calculated separately, in accordance with the values of their respective table. Figures are rounded off to the same number of decimal places as the values in the table.

Calculation of the unit cost

Each family of products has a specific calculation formula for exchange fees and for the variable registration fee, with the results valid for all of the family’s contracts.

The unit cost is calculated applying the value of the average value cost in the formula, as well as the several factors, as described below. Although the average cost formula is the same for the whole family, the final unit cost can be different, depending on the factors applied to each contract. At each stage, the unit cost of the exchange fees and variable registration fee shall be rounded off to two decimal places.

Application of the day trade incentive policy

There is a price reduction on day trades, in percentage form, which shall be directly applied to the unit cost of the exchange fees and variable registration fee of the contract, all calculated in accordance with the previous items. The result of the multiplication shall also be rounded off to two decimal places.

Exchange fee and registration fee

The exchange fee and registration fee are calculated on a per-trade basis from the unit cost for each investor, for each contract in each family, after application of the day trade incentive policy (if applicable).

Exchange fees

Unit cost of the exchange fees, multiplied by the number of contracts of each executed trade, rounded off to two decimal places.

Registration fee

The fixed registration fee is a fixed value applied per contract. The previously calculated unit cost of the variable registration fee is added to the fixed registration fee, maintaining the seven decimal places. Then the value is multiplied by the number of contracts of each executed trade, rounding off the result to two decimal places.

Foreign currency conversion

The values of the fixed registration fee in U.S. Dollar shall be converted into Brazilian Reals using the sell PTAX rate of the last day of the previous month. The result shall be rounded off to seven decimal places.

For nonresident investors trading in accordance with CMN Resolution 2687, the value of the exchange fees and registration fee will be converted into U.S. Dollars by the sell PTAX rate of the last business day of the previous month and rounded off to two decimal places.

Settlement fee

Applicable to listed derivatives, except options and spot, upon closeout of positions in the contract month.

The settlement fee is a value fixed per contract. It is multiplied by the number of settled contracts, rounded off to the second decimal place.

Permanence fee

Calculated per contract, in accordance with values established in the price tables. Its calculation basis is the number of open interest futures contracts on the previous day and represents the sum of all open interest in the same commodity and in the same market, regardless of the contract month, per account. The calculation period is the last business day of the antepenultimate month to the current one. It is calculated daily and charged as follows.

- Last business day of each month: the debit on this date will correspond to the accumulation of all the values of the permanence fee calculated on the days between the last charge and the previous business day.

- On the day following the closeout of all the positions in the same commodity of the same customer (account). In this way, the fee is debited on days between the last charge and the previous business day, exclusively for the commodity whose position was closed out.

- When there is full transfer of the positions of the customer (account) in the same commodity to another participant.

Where:

p = daily value of the permanence fee;

CAt-1 = sum of the quantity of open interest constracts on the previous day (t-1);

λ = reduction factor;

Ct + Vt = sum of the traded contracts (buy and sell, not netting) on date t;

Rounded off to the second decimal place.

For contracts with permanence fee in other currencies or commodities contracts, operated by 2687 investors (non-resident investores with CVM document), the permanence fee will be converted to BRL by the Exchange Rate from the last business day of the previous month, rounded in three decimal places.